[Industry depth] Insight 2024: Competition Pattern and market share of China's Medical imaging equipment industry (with market share, competition status summary, etc.)

Core data: Market share of medical imaging equipment industry

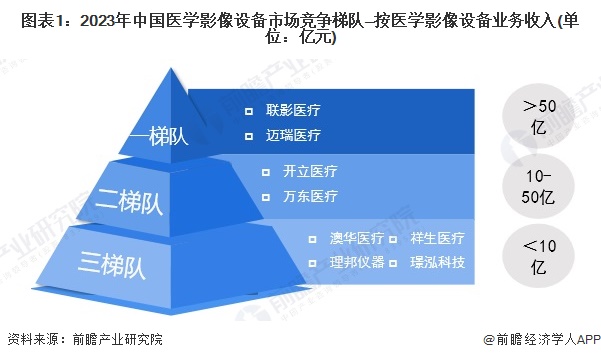

1, China's medical imaging equipment industry competition echelon

As a high-end medical device product, medical imaging equipment has high technical barriers and is one of the fastest growing disciplines in clinical medicine, with fast development and short renewal cycle. According to the business income division of medical imaging equipment industry enterprises in 2023, it can be divided into three competitive echelons. From the perspective of relevant business income of Chinese medical imaging equipment representative enterprises, Lianying Medical and Mindray Medical income exceeds 5 billion yuan, which is the first echelon; Opening medical and Wandong medical business revenue of more than 1 billion yuan, in the second echelon; Aohua Medical and other related business revenue is less than 1 billion yuan, located in the third tier.

2, China's medical imaging equipment industry concentration

Overall, China's medical imaging equipment industry market concentration is low, although the leading enterprises market business revenue is higher, but compared to the entire market, the proportion is relatively small, CR2 total 26.88%. Lower revenue from other corporation-related businesses led to low market concentration, with 31.82% for CR4 and only 34.41% for CR8.

3, China's medical imaging equipment industry enterprise layout

Among the listed companies in the medical imaging equipment industry, the opening of medical imaging equipment business accounts for the largest proportion of business revenue, and the business is relatively concentrated. In terms of regional layout, most companies of medical impact equipment have a layout at home and abroad, of which Xiangsheng Medical overseas business layout accounts for the largest proportion; In terms of research and development investment, Xiangsheng Medical research and development investment accounts for the largest proportion of operating income.

4. Summary of competition in China's medical imaging equipment industry

From the analysis of Porter's five forces model, China's medical imaging equipment industry in the low-end product market, a large number of domestic manufacturers, fierce competition, and high-end medical imaging equipment mainly concentrated in foreign enterprises; At present, China's medical imaging equipment industry faces high qualification, talent and technical barriers, the industry entry threshold is high, and the threat of new entrants is relatively general; At present, there are no effective alternative products for medical imaging equipment products, and the external competition mainly comes from imported products. The upstream industry mainly provides parts, raw materials and other basic products for the medical imaging equipment industry, and the size of suppliers varies, and the industry is developing rapidly and the industry is relatively mature, but the core components still rely on imports, so the industry has a general bargaining power on the upstream; Medical imaging equipment products do not have alternative products, and the downstream bargaining power is higher, and the overall bargaining power of medical imaging equipment is higher on the downstream industry.

Porter's "five forces" model is used to analyze the competitive environment of the medical imaging equipment industry, and the competition in all aspects is quantified, with 5 representing the maximum and 0 representing the minimum. The competition in the medical imaging equipment industry is shown as follows:

|

Last:Reprint:Medical insurance fund to medical institutions instant settlement reform

Next:Reprint:The NHC is responsible for the national key research and development program |

Return |

Mobile website